Affordable Tail Insurance for Physicians

Recruiting top-tier physicians is essential for any thriving healthcare organization. To compete with large, well-capitalized health systems, you must present a competitive offer. However, the true cost of recruitment extends far beyond salary and signing bonuses. It must also contemplate the significant future expense of physician tail coverage, a critical component of medical malpractice tail insurance.

This looming financial obligation can make aggressive physician recruitment feel like a strategic risk.

But what if there were a smarter way? A strategy that allows your organization to compete for talent actively while managing current premium costs and responsibly funding the essential long-term protection for those physicians after they depart?

Well. There is.

This article introduces a powerful tool in Healthcare Medical Professional Liability Insurance, labelled the Scheduled Doctors Endorsement. It is an approach that is increasingly structured and implemented by specialized firms such as The Doctors’ Insurance Agency, which we will explore in more detail.

For smaller and mid-sized healthcare organizations, this challenge is even more acute. Unlike large, well-capitalized health systems that can absorb six-figure tail liabilities as a cost of scale, independent practices and regional groups must manage physician recruitment costs with far greater precision. A scheduled doctors’ endorsement helps level this playing field by transforming tail insurance from a destabilizing exit cost into a controlled, ongoing component of risk management.

What Is Tail Insurance for Physicians?

Appreciating the benefits of scheduled endorsements requires understanding the underlying issue they resolve. Physician tail coverage, technically termed Extended Reporting Period (ERP) protection, functions as an indispensable element of claims-made malpractice insurance structures.

Under a claims-made policy, coverage is triggered only if a claim is filed while the policy is active. When a physician leaves a practice, their coverage ends. However, patients can file medical liability claims years after the actual incident occurred. Tail coverage protects claims reported after the physician's policy terminates, but for incidents that happened during the active policy period. This addresses physician liability after termination, a fundamental concern in medical liability risk management.

But then again, who assumes the financial burden of Tail Insurance upon a physician's departure?

This question consistently ranks among the most contentious items in employment contract negotiations. Clarity on this challenge creates opportunity for more innovative solutions.

Introducing the Schedule of Physicians' Endorsement

The schedule of doctors' endorsement, which is also known as a blanket physician endorsement or roster malpractice policy, transforms the tail insurance equation. This is achieved through a structure designed explicitly to help healthcare organizations contain and manage the long-term cost of tail insurance.

In essence, your organization is able to add recruited physicians to your master healthcare professional liability insurance policy via a schedule. The process is streamlined for easy underwriting. Typically, you'll complete a concise physician application, provide a CV, and submit a recent claims history report. The NPDB claims report (National Practitioner Data Bank) can often be obtained within minutes, significantly speeding up the process.

This streamlined underwriting process offers a strategic advantage. By reducing administrative friction, healthcare organizations can onboard physicians more efficiently, support accelerated recruitment timelines, and avoid delays that often arise from separate policy negotiations.

Once physicians are added to the schedule, the financial structure becomes even more compelling.

Affordability Meets Robust Protection: A Shared Limit Concept

The power of this structure lies in its shared limit malpractice policy design. The policy features a single aggregate limit shared by all physicians on the schedule, yet it also provides a dedicated per-claim limit for each doctor.

Through this approach, you achieve two key goals:

- It makes premiums significantly more affordable than purchasing separate, individual policies for each physician, and

- It simplifies the underwriting process, as carriers assess the group risk. The premium adjusts competitively when a physician is added, representing a savings over the cost of a conventional separate-limit policy.

Even when multiple physicians have departed, the structure preserves sufficient per-claim protection. Because limits refresh annually and per-claim limits apply individually, coverage adequacy is maintained without erosion caused by accumulated departures.

This financial efficiency pales in comparison to the endorsement's most powerful feature: continuous post-employment protection.

Future Coverage After Termination

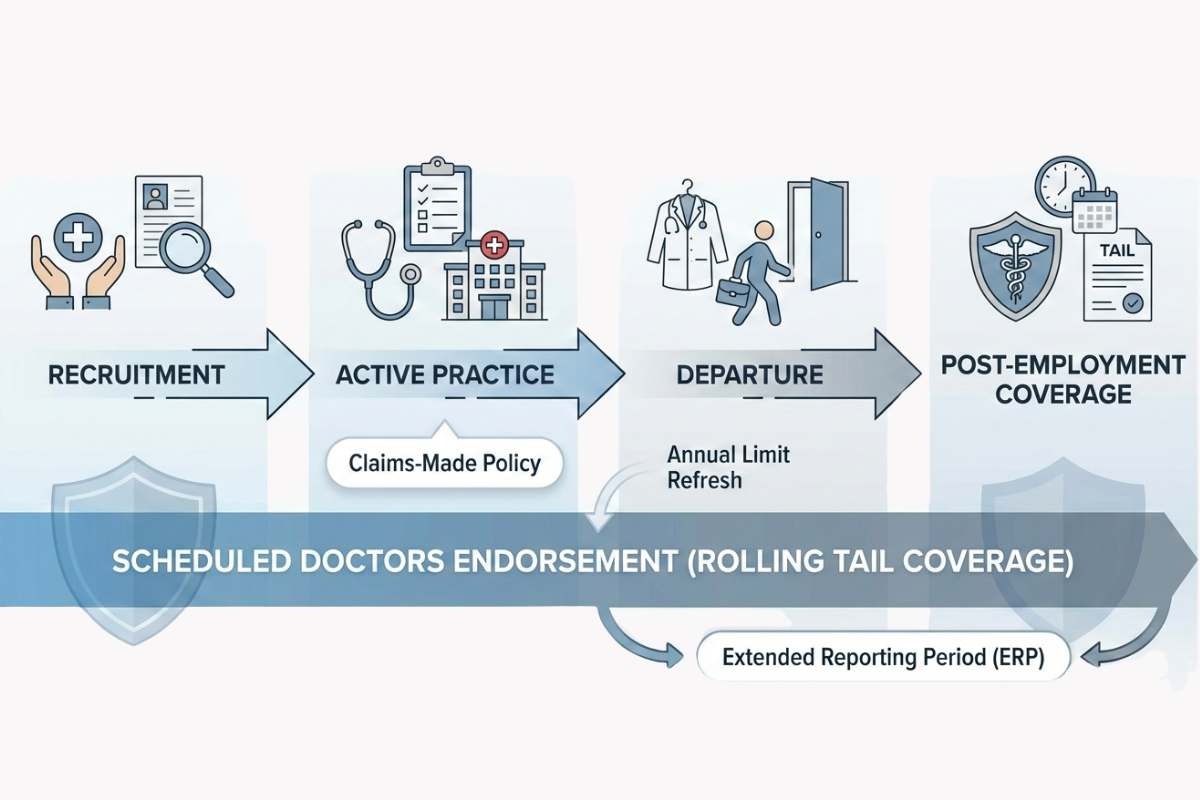

The most valuable aspect of the departed physician endorsement is its built-in mechanism for post-employment malpractice coverage. Once a physician on the schedule terminates, the associated premium doesn't vanish entirely. Rather, it diminishes actuarially, reflecting the decaying risk of a claim being filed.

This premium adjustment is an intentional actuarial glide path. As time passes and the probability of a claim diminishes, the retained premium is reduced accordingly, allowing the carrier to sustain long-term protection while preventing unnecessary cost retention for the organization.

Critically, the physician remains on the schedule with a termination date noted. This ensures the insurance carrier remains responsible for any future claims arising from their period of active coverage.

The carrier holds the "tail," providing a continuous extended reporting period (ERP), which is a standard actuarial tail risk calculation built into the policy.

This structure represents a contractual commitment by the insurance carrier, not a discretionary accommodation. Recording termination dates within the schedule also functions as an active risk-management control, allowing carriers and organizations to align premium adjustments with exposure timelines.

Continuous protection of this nature is further enhanced by the policy's annual renewal structure.

Refreshed Limits and Continuous Protection

Perhaps the most significant financial advantage is the annual reset. Each year, when your master policy renews, the limits applicable to departed physicians are also refreshed and renewed. This approach creates a new, dedicated source of coverage for any claims made against those physicians in that new policy year.

Instead of purchasing an expensive, standalone individual tail policy for every departing doctor, this rolling tail coverage provides a single, aggregated tail coverage that resets annually.

From a risk-transfer standpoint, this distinction is critical. The tail exposure remains with the insurance carrier, and not on the organization's balance sheet. Thus, ensuring that long-tail liabilities are fully transferred rather than informally retained.

Retaining a portion of the premium through annual renewals is not a drawback. It is the mechanism that enables continuous, refreshed protection.

This structure replaces unpredictable exit costs with a deliberate, sustainable funding model. Understanding how this approach differs from traditional methods clarifies its strategic value.

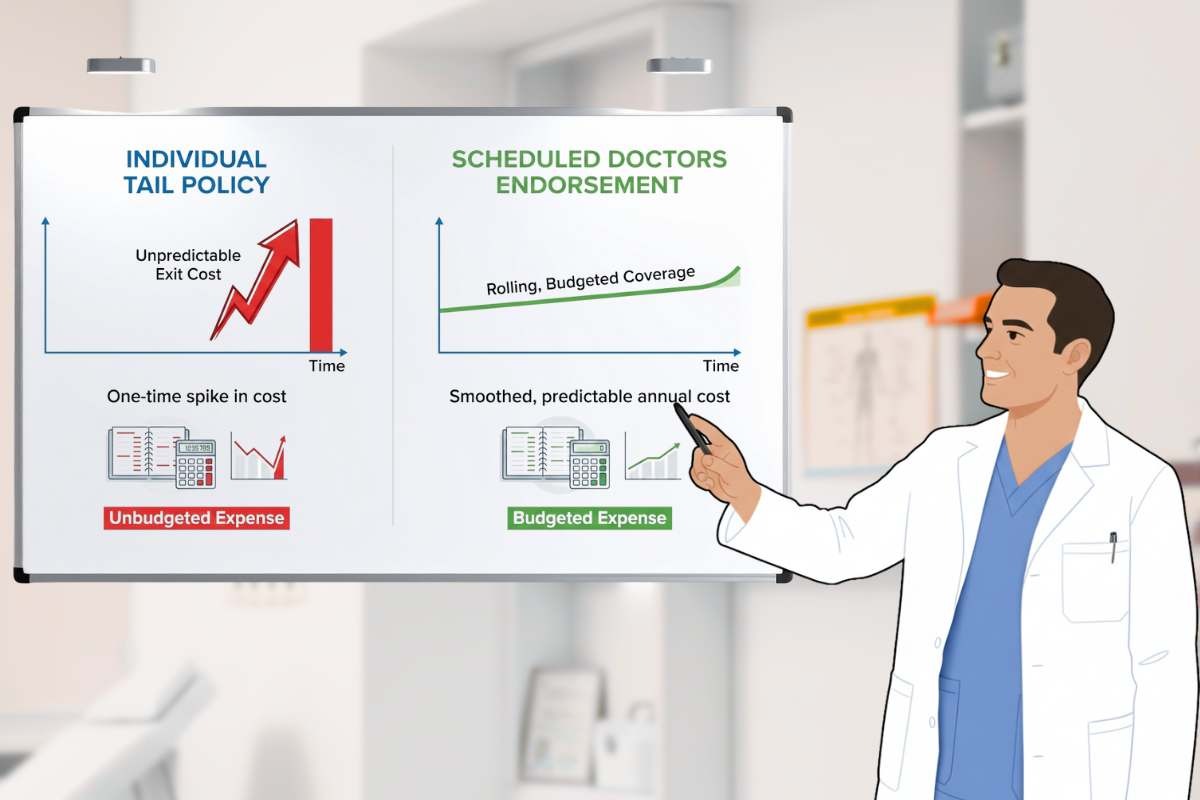

Scheduled Endorsement vs. Individual Tail Policies

- Individual Tail Policies: A one-time, often five or six figgure premium paid when a physician leaves. This cost is unpredictable, can strain budgets, and creates a number of separate policies to administer.

- Scheduled Doctor Endorsement (Rolling Tail): A manageable, built-in cost spread over time through annual policy renewals. It provides rolling tail coverage that offers continuous, refreshed limits for all departed schedule members, simplifying administration and enhancing financial predictability.

Administratively, this approach eliminates the burden of tracking multiple individual tail policies over years or decades. Coverage remains centralized within the master policy, reducing documentation complexity and long-term compliance risk.

Beyond individual physician protection, this structure also safeguards the organization itself.

Covering Vicarious Liability through Comprehensive Liability Protection

A strategic and organized structure offers robust, ongoing protection for the healthcare organization itself. Importantly, scheduled endorsement provides vicarious liability coverage, meaning the organization remains protected if it is named in a lawsuit alongside its physicians, current or former.

Unlike traditional policies that trigger a separate tail purchase at each cancellation, this method integrates physician termination tail coverage into the holistic policy renewal.

As a unified approach, it ensures complete liability protection for both the individual departing physicians and the organization, supporting a sound physician retention and risk strategy.

A Smarter Approach to Physician Tail Coverage

The schedule of physicians' endorsement transforms physician tail coverage from a capital-intensive expense into a predictable, managed cost. By leveraging this blanket physician endorsement, your organization can make more competitive recruitment offers while protecting its long-term financial health against long-tail medical liability claims.

At The Doctors' Insurance Agency, we specialize in structuring affordable tail insurance for physicians through innovative solutions like the scheduled endorsement. Ready to explore the strengthening impact of a roster malpractice policy on your organization's foundation? Contact us for a detailed tail insurance cost comparison.

The Doctors' Insurance Agency properly insures the people and organizations of medicine