How Retroactive Date in Claims-Made Medical Malpractice Insurance Protects Your Entire Career

For physicians, surgeons, mid-level providers, and advanced practice clinicians, navigating the complexities of medical professional liability insurance is as important as patient care itself.

At the heart of this protection lies a single, often overlooked information: The date on your policy declarations page, which is referred to as the retroactive date.

Understanding and preserving this date is critical to maintaining an unbroken chain of malpractice insurance, safeguarding your career and finances from unforeseen legal exposure.

At The Doctors’ Insurance Agency, we specialize in helping MDs, DOs, and advanced practice clinicians understand and maintain continuous claims-made Medical Malpractice Insurancecoverage, protecting both their past acts and future career transitions.

This article will guide you through all the essential mechanics, explain the peril of coverage gaps, and provide a clear roadmap for ensuring continuous protection throughout every career transition.

What Is a Claims-Made Medical Malpractice Insurance Policy?

Most physician malpractice insurance coverage is written on a claims-made basis.

But what does this truly mean?

Unlike other insurance you may be familiar with, a claims-made policy provides coverage only if the policy is in force, both when the incident occurs and when the claim is filed.

This is fundamentally different from occurrence malpractice insurance, which covers any incident that happens during the policy period, regardless of when the claim is later reported.

Think of it this way: your homeowner or auto insurance covers real-time risks. If you cancel it, you’re simply no longer insured for future incidents.

Medical malpractice insurance protection, however, depends on an uninterrupted sequence of coverage because claims can arise years after care was provided. Cancelling a claims-made policy without a plan for future claims is where dangerous coverage gaps begin.

Why the Retroactive Date Matters: Secure Your Protection

Retroactive date is the linchpin of your claims-made policy. This date is listed on your malpractice insurance declarations page and signifies the start of your continuous coverage.

Any act or omission occurring on or after this date is eligible for coverage, provided the policy is active when the claim is made.

The critical concept is this: You can be sued today for care you provided five years ago.

But if your current policy’s retroactive date goes back at least five years, you’re protected.

If a coverage gap has reset that date, you are personally liable for that claim. This is prior acts coverage in action, and it’s non-negotiable for secure medical liability insurance continuity.

Additionally, medical malpractice insurance premiums are not static.

Rates fluctuate as claims frequency increases, average settlement values rise, and carriers respond to broader litigation trends. Premiums may also change based on geographic location, expanded procedures, added surgical services, or shifts in the scope of practice.

In this environment, preserving your original retroactive date serves as a stabilizing influence, signalling continuity and predictability to insurers even as external market pressures evolve.

Beyond coverage mechanics, a continuous retroactive date communicates disciplined risk management to underwriters.

Physicians who maintain uninterrupted claims-made coverage are viewed as more stable risks, even when premiums increase for reasons unrelated to individual performance. Losing that continuity does not merely reset coverage; it alters how carriers evaluate you going forward.

Claims-Made vs. Occurrence Policies Explained

Let’s clarify the key distinction:

- Claims-Made Policy: Covers claims made and reported while the policy is active. It is typically less expensive upfront but requires active management of the retroactive date and may necessitate purchasing tail coverage upon cancellation.

- Occurrence Policy: Covers any incident that occurred during the policy period, even if the claim is filed years later. This policy effectively has the cost of tail coverage built into each premium, making it more expensive initially but simpler.

Many employed physicians at large institutions are covered by occurrence policies, leading to the common and costly misconception that a private claims-made policy works “the same way.”

This assumption can lead to catastrophic errors when cancelling coverage.

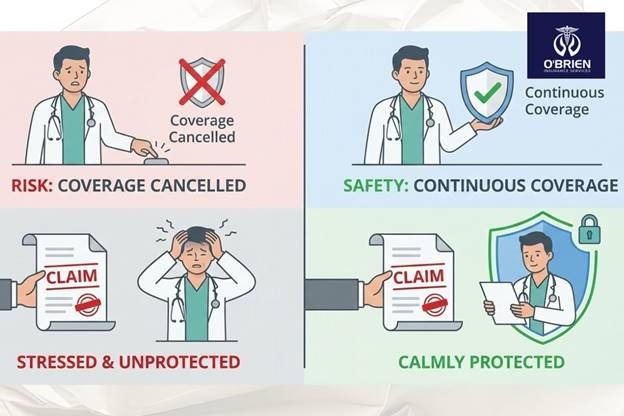

What Happens If You Cancel a Claims-Made Policy?

Cancelling a claims-made malpractice insurance policy leaves physicians exposed. Any lapses create a "bare period," after which you cannot simply reinstate prior acts coverage. Carriers view going bare as a significant risk indicator.

Critical Warning: Downtime is not insurable.

Once you cancel, you cannot later obtain a new policy that covers the past. Insurance companies will not allow physicians to selectively insure retroactive exposure only when they fear a claim.

One of the most common ways physicians unintentionally create coverage gaps occurs during part-time or supplemental work.

Physicians employed full-time by hospitals, universities, or large medical groups often carry a separate claims-made policy for moonlighting or side practice activities. When that work ends, many assume they can simply cancel the policy, not realizing that doing so without tail coverage leaves prior acts permanently uninsured.

If you leave a practice or cease part-time work, you generally have two options to avoid a gap:

- Continue paying the premium to keep the policy active.

- Purchase tail coverage from your current carrier.

Understanding Tail Coverage and Extended Reporting Periods

Medical Malpractice Tail coverage, formally known as an extended reporting period endorsement, is a one-time purchase that extends your policy’s reporting window indefinitely after cancellation.

It permanently covers prior acts back to your retroactive date.

However, tail insurance costs for physicians are substantial at an average of about 150% to 200% of your annual premium, with no financing options.

While some carriers offer a permanent tail malpractice insurance option, it’s considered a significant, upfront expense. Hence, the smarter financial and risk-management strategy is to avoid needing a tail until absolutely necessary (e.g., at retirement).

Many physicians resist purchasing tail coverage because they feel they are paying for a policy they are “no longer using.” This is a dangerous misconception. A tail policy is actively protecting prior acts for which claims may arise years—or even decades—later.

In reality, the physician is still “using” the policy to cover work already performed.

How to Transfer Your Policy and Preserve Your Retroactive Date

When changing jobs, this is the most important question to ask a new employer or practice manager: “Can I transfer my current claims-made policy with its existing retroactive date to this group?”

If the answer is yes, it is the ideal scenario. There are several advantages attached to the practice of transferring malpractice insurance between practices:

- Prevents the need for you to purchase an expensive tail from your prior carrier.

- Spares your prior practice from potential tail cost obligations.

- Maintains your unbroken chain of malpractice insurance, keeping your original retroactive date intact.

This seamless transfer is the gold standard for malpractice insurance during job transition and a key service we facilitate at The Doctors’ Insurance Agency.

The Long-Term Risk of Going Bare in The E&S Market

Allowing your policy to lapse doesn’t just create exposure; it can permanently alter your insurance standing. When a physician is uninsured at the time a claim is filed, there is no carrier obligation to defend.

This means personally funding legal counsel, expert witnesses, court costs, and settlement negotiations. These are expenses that can easily reach six or seven figures regardless of the claim outcome.

Admitted malpractice insurance carriers are often the most competitively priced, and they typically refuse to insure physicians with a recent bare period.

From an underwriting perspective, going bare is not viewed as a neutral event but as a failure of professional risk management. As a result, admitted carriers will generally decline to cover both prior acts and future exposure for physicians who have allowed coverage to lapse.

They see it as an irresponsible action and will neither cover prior acts nor future exposure.

Fortunately, the Excess and Surplus Lines (E&S) medical malpractice insurance market exists for this reason.

It is important to understand that the E&S market is not inherently punitive or disreputable. Many surplus lines carriers are conservatively financed, well-established, and widely respected within the medical malpractice industry.

These policies are common and legitimate solutions for physicians with unique risk profiles, though they are typically more expensive and less flexible than coverage available in the admitted market.

Surplus lines carriers provide a vital niche for physicians who:

- Have a malpractice insurance lapse.

- Forgot to purchase a tail policy.

- Have a frequency of claims or disciplinary history.

- Need coverage after a gap.

- Have experienced medical board administrative actions, consent orders, or regulatory judgments, even in the absence of paid malpractice claims.

While the E&S market offers essential options and is filled with reputable, well-financed carriers, policies are generally more expensive and may have different terms than the standard admitted market. For specialties like OB/GYN or pediatrics, where long statutes of limitations apply, avoiding this market through continuous coverage is paramount.

Protecting Your Career Journey: Have a Plan

The statute of limitations for medical malpractice is not a simple timer. With the discovery rule, the clock often starts when the patient discovers an injury, not when the care was rendered.

For minors, the clock may not start until they turn 18, meaning a pediatrician could be sued for an act two decades prior.

My final words are on proactive planning.

Maintaining an unbroken chain of malpractice insurance is a non-negotiable pillar of your career.

Many physicians are never explicitly taught how claims-made coverage works, despite it being the dominant malpractice insurance structure in private practice. As a result, the retroactive date, which is one of the most critical elements of protection, is often misunderstood until irreversible damage has already occurred.

It ensures you are protected against the long-tail nature of malpractice claims filing timelines, provides peace of mind, and preserves your access to the broadest, most affordable insurance markets.

At The Doctors’ Insurance Agency, we specialize in helping Medical Doctors, DOs, and advanced practice clinicians navigate these critical decisions. We ensure your medical professional liability insurance moves with you, protecting your past as you build your future.

Don’t let a coverage gap dictate your options. Consult with a licensed insurance professional at The Doctors’ Insurance Agency for guidance specific to your situation today, and secure your legacy.